Understanding the 7 Types of Budgets in India

Table of Contents

Understanding the Types of Budgets in India

Union Budget

Understanding the Types of Budgets in India . The Union Budget is a financial plan presented by the government that outlines the expected income and expenses for the coming year. It is an important event as it impacts various aspects of the economy, such as taxes, government spending, and public welfare schemes.

Here is a simplified explanation of the key elements of the Union Budget:

- Income: This includes the money the government expects to earn from taxes (like income tax, corporate tax, and GST), non-tax revenues (like profits from public sector companies), and other sources.

- Expenses: This covers the money the government plans to spend on various services and projects. Major areas include defense, education, healthcare, infrastructure, and subsidies.

- Deficit: Sometimes, the government’s expenses are more than its income. This difference is called the fiscal deficit. The government borrows money to cover this gap.

- Key Announcements:

- Tax Changes: The budget may introduce new taxes, change existing tax rates, or provide tax relief to certain groups.

- Welfare Programs: Announcements of new or expanded schemes for healthcare, education, agriculture, and social welfare.

- Infrastructure Projects: Plans for building roads, bridges, airports, and other infrastructure.

- Economic Reforms: Measures to improve the business environment, attract investment, and boost economic growth.

- Impact on People: The budget affects everyone. For example, changes in income tax rates can impact your take-home pay. Increased spending on healthcare or education can improve public services.

2. State Budget

Each of India’s states has its own budget, which is presented by the respective state finance ministers in the state legislatures. The State Budget operates similarly to the Union Budget but is focused on the revenue and expenditure of the state governments. It plays a critical role in addressing the unique needs and priorities of individual states, such as agriculture, local infrastructure, and social welfare programs.

3. Plan Budget

The Plan Budget is a specific part of the Union and State Budgets that focuses on the allocation of funds for development programs and schemes outlined in the Five-Year Plans. Though India no longer follows the Five-Year Plan framework, the concept of planned expenditure continues in various forms, aimed at long-term development goals. It covers areas like infrastructure projects, social sector schemes, and economic development initiatives.

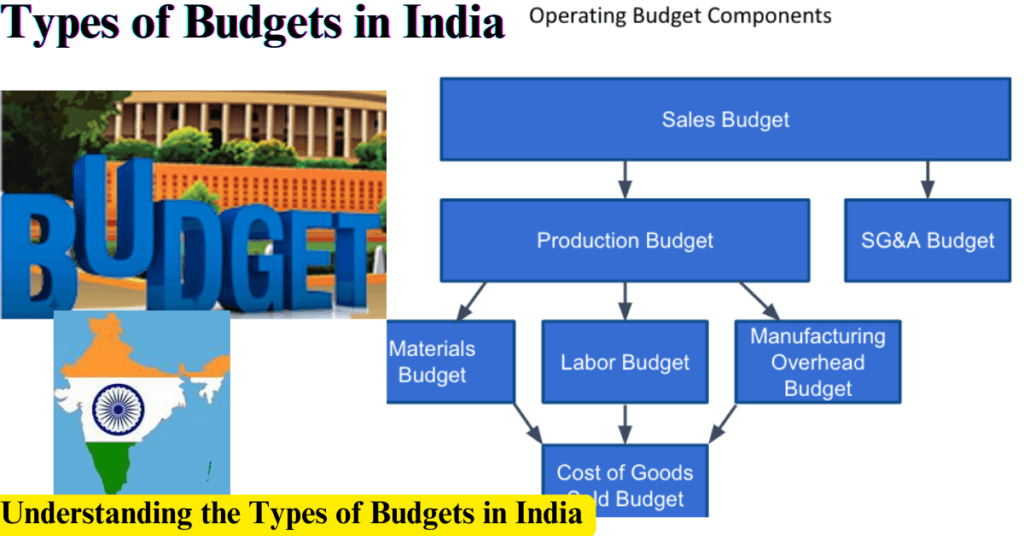

4. Performance Budget

A Performance Budget provides detailed information on the objectives, programs, and activities of various government departments and ministries. It links the financial outlay to the measurable outcomes and performance indicators, ensuring accountability and transparency in government spending. This type of budget helps in assessing the effectiveness and efficiency of government programs.

5. Supplementary Budget

During a fiscal year, unforeseen circumstances or additional expenditures may arise that were not accounted for in the original budget. In such cases, the government presents a Supplementary Budget to seek Parliament’s approval for additional funds. This budget ensures that the government can meet its financial obligations without disrupting planned activities.

6. Vote-on-Account

A Vote-on-Account is a temporary financial arrangement that allows the government to cover its expenses for a short period, usually until the full budget is passed. This provision is used when the budget is not passed before the start of the new fiscal year, ensuring continuity in government operations. It is typically used during election years or in special circumstances.

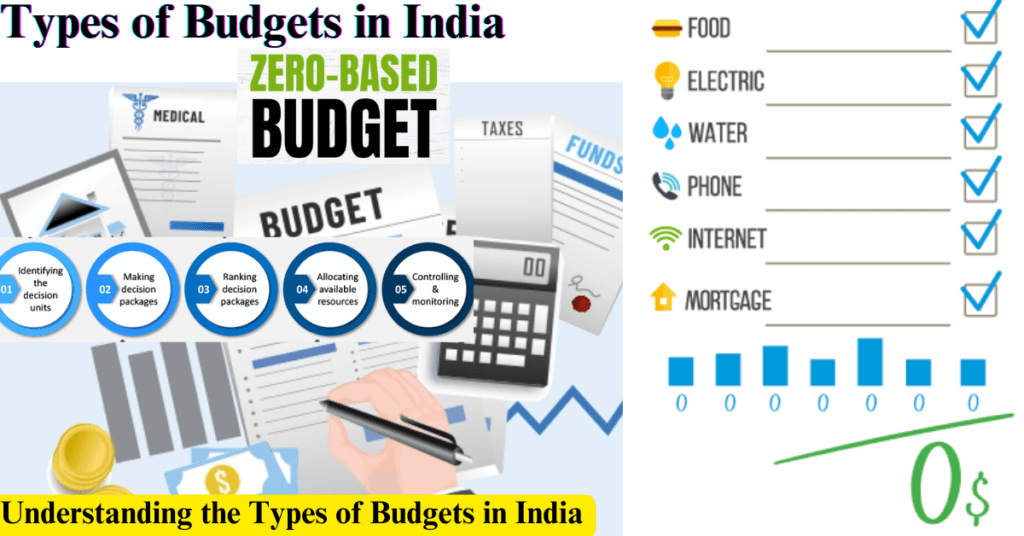

A Simple Guide to Zero-Based Budgeting

Zero-Based Budgeting (ZBB) is a method where every budget cycle starts from zero, requiring a fresh justification for all expenses. Unlike traditional budgeting, which adjusts last period’s budget, ZBB demands a thorough review of every cost.

What is Zero-Based Budgeting?

Zero-Based Budgeting is a financial strategy where each budgeting period begins with no pre-approved budget. Instead, every expense must be newly justified, regardless of what was spent previously.

Core Principles of Zero-Based Budgeting

- Begin Anew: Every period starts from zero, with no reliance on past budgets.

- Justify All Costs: Each expense must be explained as though it is being requested for the first time.

- Focus on Priorities: Funds are allocated based on current needs and priorities, ensuring alignment with organizational goals.

How to Implement Zero-Based Budgeting

- Define Decision Units: Divide your organization into units (departments, teams, projects) for budget consideration.

- Assess Needs and Costs: Examine each unit’s needs and associated costs. Document and analyze every expense.

- Justify Each Request: Each unit must provide a rationale for their budget needs, showing how they support organizational objectives.

- Review and Approve: A committee reviews the budget requests, prioritizes them, and approves the most necessary and justified expenditures.

- Allocate Funds: Distribute resources based on the approved justifications, ensuring effective use of the budget.

Advantages of Zero-Based Budgeting

- Cost Savings: Helps identify and cut unnecessary costs by requiring a fresh review of every expense.

- Effective Resource Use: Allocates funds to activities that align with current priorities and goals.

- Flexibility: Adapts to current needs rather than relying on historical spending patterns.

- Increased Accountability: Demands detailed justification for all expenses, fostering transparency.

Challenges of Zero-Based Budgeting

- Time and Effort: The process of justifying every expense can be time-consuming and labor-intensive.

- Complexity: Managing detailed budget requests can be challenging, especially in larger organizations.

- Resistance: There may be pushback from those used to traditional budgeting methods.

Conclusion

Understanding the Types of Budgets in India .The different types of budgets in India reflect the country’s complex economic landscape. From the comprehensive Union Budget to the detailed Performance Budget, each type serves a specific purpose in managing the nation’s finances. Understanding these budgets helps in knowing how the government allocates resources, plans for development, and ensures fiscal responsibility. As India evolves, its budgeting practices will continue to shape the country’s economic future